Understanding your monthly credit card statement is essential for maintaining financial health and avoiding costly mistakes. Each month, credit card issuers send detailed documents that contain far more information than just your balance. These statements serve as comprehensive financial records that track spending patterns, calculate interest charges, and provide legal documentation for tax purposes and dispute resolution. Whether you receive paper statements in the mail or digital versions through online banking, knowing how to interpret every section empowers you to make informed decisions about your money.

Anatomy of Your Monthly Credit Card Statement

Every monthly credit card statement follows a standardized structure designed to meet regulatory requirements while providing cardholders with essential information. The format may vary slightly between issuers, but core components remain consistent across the industry.

Account Summary Section

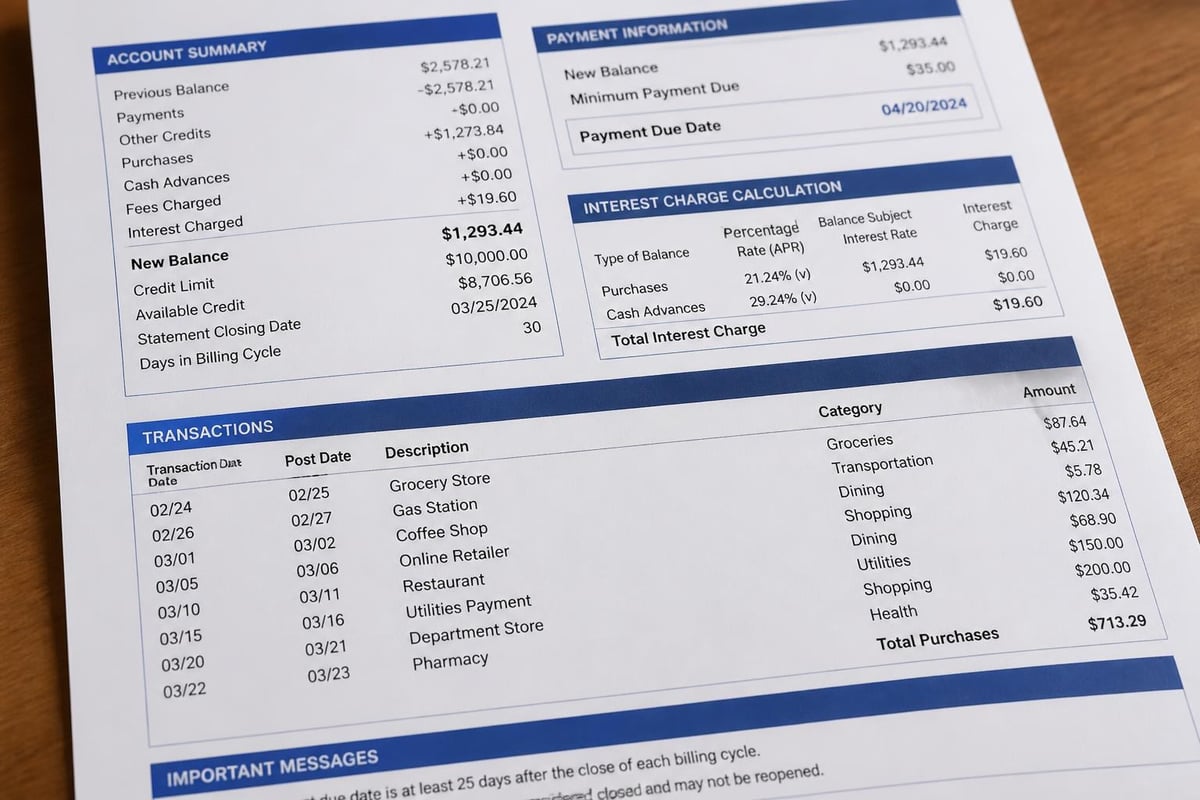

The account summary appears prominently at the top of your statement and delivers the most critical information at a glance. This section includes your previous balance, new balance, available credit, and credit limit. You'll also find your minimum payment amount and the payment due date clearly displayed.

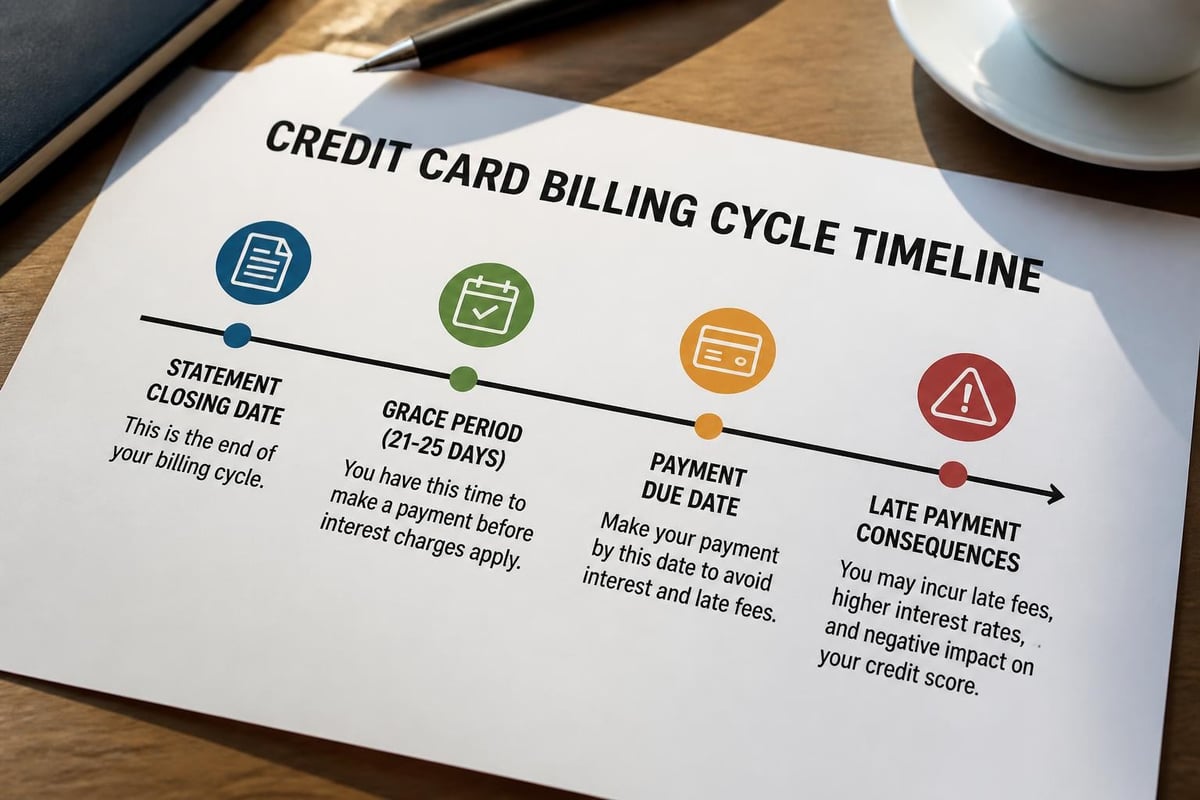

Your statement closing date marks the end of the billing cycle and determines which transactions appear on each statement. Understanding how to read credit card statements helps you track your spending cycles accurately.

Key details in the account summary:

- Previous balance: Outstanding amount from last month

- Payments and credits: Money applied to your account

- Purchases and adjustments: New charges during the cycle

- Fees charged: Late fees, annual fees, or other penalties

- Interest charged: Finance charges on unpaid balances

- New balance: Total amount currently owed

Transaction History Details

The transaction history section provides a chronological record of every purchase, payment, credit, and fee during the billing cycle. Each entry typically includes the transaction date, post date, merchant name, and amount.

Review this section carefully to verify all charges are legitimate. Fraudulent transactions often appear here first, making regular statement review your primary defense against unauthorized use. According to Experian's guidance on statement reading, catching errors early significantly improves dispute resolution success rates.

Transactions are commonly organized by category:

- Purchases: All merchant transactions

- Cash advances: ATM withdrawals and cash-equivalent transactions

- Balance transfers: Amounts transferred from other cards

- Payments: Your submitted payments

- Credits: Refunds and statement credits

- Fees: Service charges and penalties

Interest Rates and Finance Charges Explained

Understanding how interest accumulates on your monthly credit card statement is crucial for minimizing costs. The Annual Percentage Rate (APR) represents the yearly interest rate, but credit card companies calculate charges daily using the daily periodic rate.

APR Variations on Your Statement

Most statements display multiple APR categories because different transaction types carry different rates. Your purchase APR applies to regular spending, while cash advance APR (typically higher) applies to ATM withdrawals. Balance transfer APR governs transferred balances, and penalty APR may apply if you miss payments.

| Transaction Type | Typical APR Range | Grace Period |

|---|---|---|

| Purchases | 16% - 24% | Yes (if paid in full) |

| Cash Advances | 25% - 30% | No |

| Balance Transfers | 0% - 18% (promotional) | No |

| Penalty Rate | 29.99% | No |

The comprehensive breakdown from Bankrate demonstrates how these rates compound when balances carry over month to month.

Calculating Your Finance Charges

Finance charges appear as a separate line item on your statement. Credit card issuers calculate these charges using your average daily balance, which factors in daily fluctuations from purchases and payments throughout the billing cycle.

Average daily balance calculation: The issuer adds your balance for each day of the billing cycle, then divides by the number of days in the cycle. This amount multiplied by the daily periodic rate (APR ÷ 365) and the number of days in the cycle equals your finance charge.

Payment Information and Minimum Payment Warnings

The payment information box on your monthly credit card statement contains federally mandated disclosures designed to protect consumers from the long-term costs of minimum payments.

Minimum Payment Breakdown

Your statement must show three critical pieces of payment information. First, the minimum payment due represents the smallest amount you can pay to keep the account in good standing. Second, a warning explains how long it will take to pay off your balance making only minimum payments. Third, a calculation shows how much you should pay monthly to eliminate the debt within three years.

This disclosure often surprises cardholders when they see the dramatic difference in total costs:

- Paying minimum only: May take 20+ years and double your original balance

- Paying three-year amount: Saves thousands in interest charges

- Paying full balance: Eliminates all interest charges completely

Capital One's statement reading guide emphasizes these payment scenarios to help cardholders make informed decisions.

Payment Due Date and Grace Periods

The payment due date appears prominently on every monthly credit card statement. Missing this deadline by even one day can trigger late fees ranging from twenty-five to forty dollars, plus potential penalty APR increases.

The grace period (typically 21-25 days) represents the time between the statement closing date and payment due date. During this window, you can pay your balance in full without incurring interest charges on new purchases.

Rewards Summary and Benefits Tracking

Many monthly credit card statements include a dedicated section for rewards programs, making it easier to track earned benefits. This section displays points earned, miles accumulated, cashback percentages, and redemption options.

Understanding Your Rewards Statement

Your rewards summary typically shows:

- Points or miles earned during the current statement period

- Year-to-date totals

- Available balance for redemption

- Bonus category earnings

- Expiration dates for promotional rewards

Track these rewards carefully to maximize value. Some programs offer enhanced redemption rates for specific uses, while others devalue points over time or impose expiration dates.

For businesses managing multiple credit cards, converting these statements to spreadsheet format streamlines rewards tracking across all accounts. Using a PDF bank statement to spreadsheet conversion service helps consolidate this data for comprehensive analysis.

Fees and Penalties Section

Every monthly credit card statement must clearly disclose all fees charged during the billing cycle. These charges can significantly impact your account balance if left unchecked.

Common Credit Card Fees

Understanding fee structures helps you avoid unnecessary charges:

- Annual fees: Yearly membership costs (often waived first year)

- Late payment fees: Charges for missing due dates ($25-$40)

- Foreign transaction fees: Percentage charged on international purchases (1%-3%)

- Cash advance fees: Percentage or flat fee for withdrawing cash (3%-5% or $10 minimum)

- Balance transfer fees: Percentage charged on transferred amounts (3%-5%)

- Over-limit fees: Charges for exceeding credit limit (less common after 2009 regulations)

- Returned payment fees: Penalties for insufficient funds ($25-$40)

The detailed explanation from Self provides specific examples of how these fees accumulate and strategies to avoid them.

Year-End Summary and Tax Documentation

Your December monthly credit card statement often includes an annual summary section that aggregates spending categories and fees paid throughout the year. This information proves invaluable for tax preparation, budgeting analysis, and expense tracking.

Annual Summary Components

The year-end summary typically includes:

- Total interest paid (important for business expense deductions)

- Total fees charged across all categories

- Category spending totals (dining, travel, groceries, etc.)

- Rewards earned and redeemed

- Average monthly balance

Business owners particularly benefit from this consolidated view when preparing tax returns. Interest on business credit cards may be deductible, and categorized spending helps identify deductible business expenses.

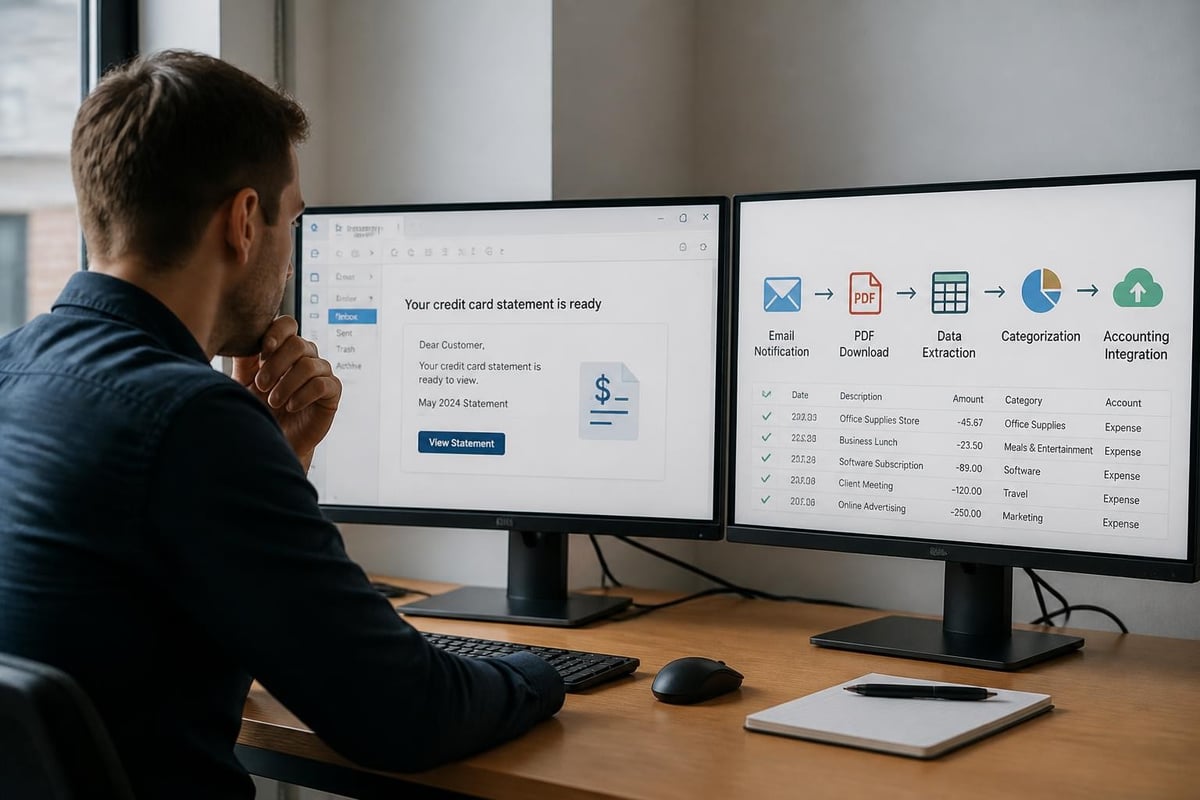

Digital Statement Access and Record Keeping

Modern monthly credit card statements are increasingly delivered electronically, offering advantages over paper versions while requiring different management strategies.

Benefits of Electronic Statements

Digital statements provide immediate access, searchable text, and integration capabilities with financial software. You can download statements as PDFs for permanent archiving, ensuring you maintain records beyond the typical online retention period of 12-24 months.

Electronic delivery also:

- Reduces identity theft risk from mail interception

- Provides instant notification when statements are available

- Enables keyword searches across multiple statements

- Facilitates easier sharing with accountants or financial advisors

- Supports automated expense tracking systems

Converting Statements for Analysis

For comprehensive financial analysis, many businesses and individuals convert PDF statements into spreadsheet formats. This transformation enables advanced sorting, filtering, and calculation capabilities that static PDFs cannot provide. Understanding bank statement format variations helps ensure successful conversions across different issuers.

Spreadsheet conversion allows you to:

- Create custom pivot tables for spending analysis

- Generate charts visualizing spending trends

- Compare expenses across multiple billing cycles

- Import data directly into accounting software

- Consolidate multiple card statements into unified reports

Automated solutions using AI technology can extract transaction data from bank PDF statements with high accuracy, eliminating manual data entry errors and saving significant time.

Credit Utilization Ratio on Your Statement

Your monthly credit card statement provides the data necessary to calculate your credit utilization ratio, a critical factor affecting your credit score. This metric represents the percentage of available credit you're currently using.

Calculating and Managing Utilization

Credit scoring models typically consider both per-card utilization and overall utilization across all revolving accounts. The formula is straightforward: divide your current balance by your credit limit, then multiply by 100.

Optimal utilization ranges:

| Utilization Level | Credit Score Impact | Recommended Action |

|---|---|---|

| 0% - 10% | Excellent | Maintain or slightly increase |

| 11% - 30% | Good | Monitor carefully |

| 31% - 50% | Fair | Pay down balances |

| 51% - 75% | Poor | Aggressive paydown needed |

| 76% - 100% | Very Poor | Immediate action required |

Credit.org's statement reading guide emphasizes monitoring this ratio monthly to maintain healthy credit scores.

Dispute Process and Error Correction

Your monthly credit card statement serves as the foundation for disputing unauthorized charges or billing errors. Federal law provides specific protections, but timing requirements are strict.

Filing a Billing Dispute

The Fair Credit Billing Act grants consumers 60 days from the statement date to dispute charges in writing. Your statement typically includes dispute contact information and procedures in the fine print.

Common disputable items include:

- Unauthorized transactions

- Incorrect charge amounts

- Charges for undelivered goods or services

- Mathematical errors in balance calculations

- Duplicate charges

- Charges for returned merchandise

When filing disputes, reference the specific statement date, transaction date, and merchant name exactly as they appear on your monthly credit card statement. Documentation from your records strengthens your position.

Statement Alerts and Notification Settings

Modern credit card issuers offer customizable alerts that complement your monthly credit card statement, providing real-time notifications about account activity between statement cycles.

Recommended Alert Configurations

Strategic alert setup helps prevent problems before they appear on your official statement:

- Large purchase alerts: Notify when charges exceed a specified amount

- Available credit alerts: Warn when approaching credit limit

- Payment due reminders: Alert 3-5 days before due date

- Statement ready notifications: Immediate access to new statements

- International transaction alerts: Flag foreign charges immediately

- Unusual activity alerts: Detect potential fraud patterns

These real-time notifications work alongside your monthly statement to provide comprehensive account monitoring. Consolidated Credit's resource discusses integrating alerts with statement review for maximum financial awareness.

Multi-Card Statement Management Strategies

Managing multiple monthly credit card statements requires systematic organization and efficient data consolidation. Businesses and individuals with several cards face challenges tracking due dates, rewards programs, and spending across different accounts.

Centralized Statement Tracking

Create a master spreadsheet or database that aggregates key information from each monthly credit card statement:

- Statement closing dates for each card

- Payment due dates (consider calendar sync)

- Minimum payments required

- Current balances and credit limits

- Rewards earned per card

- Annual fees and renewal dates

Converting multiple checking statements and credit card statements to a unified format streamlines this process considerably. Automated conversion tools can extract data from various statement formats and normalize it into consistent spreadsheet columns.

For international businesses, AI-powered tools like Boekie AI B.V. can automatically process and categorize transactions from multiple sources, integrating seamlessly with existing accounting workflows to maintain accurate financial records across various payment methods.

Security Considerations for Statement Storage

Your monthly credit card statement contains sensitive personal and financial information requiring secure storage practices. Account numbers, transaction histories, and personal identifiers create significant identity theft risks if improperly handled.

Best Practices for Statement Security

Implement these security measures for both paper and digital statements:

For paper statements:

- Shred statements before disposal (cross-cut shredders recommended)

- Store archived statements in locked cabinets

- Limit physical access to storage locations

- Consider scanning to digital format, then destroying originals

For digital statements:

- Use encrypted storage solutions

- Implement strong password protection

- Enable two-factor authentication on accounts

- Regularly backup encrypted files

- Avoid storing on unsecured cloud services

- Consider password-protected PDF conversion

When using conversion services, verify they maintain bank-level security protocols for data handling and transmission.

Business Expense Tracking with Credit Card Statements

For business owners, the monthly credit card statement functions as a primary source document for accounting, tax preparation, and financial analysis. Proper statement management directly impacts financial reporting accuracy and tax compliance.

Categorizing Business Expenses

Your monthly credit card statement provides raw transaction data that requires categorization for meaningful business analysis:

- Operating expenses: Office supplies, utilities, subscriptions

- Travel and entertainment: Client meals, lodging, transportation

- Professional services: Legal fees, consulting, software

- Marketing and advertising: Promotional campaigns, sponsorships

- Equipment and technology: Hardware, software licenses

- Inventory and supplies: Raw materials, resale goods

Converting statements to spreadsheet format allows custom categorization aligned with your chart of accounts. The ability to convert bank statements to Excel format enables seamless import into accounting platforms like QuickBooks, Xero, or FreshBooks.

Separating Personal and Business Charges

Even with dedicated business cards, personal charges occasionally appear on business monthly credit card statements. Accurate separation is essential for tax compliance and prevents audit complications.

Spreadsheet conversion facilitates this segregation through:

- Custom columns for expense classification

- Filter functions to isolate personal transactions

- Percentage calculations for mixed-use expenses

- Documentation notes linked to specific transactions

- Year-end summary reports showing business-only totals

Statement Reconciliation with Accounting Records

Monthly reconciliation between credit card statements and accounting records identifies discrepancies, prevents fraud, and ensures financial accuracy. This process verifies that every transaction recorded in your books matches the official statement.

Reconciliation Steps

Follow this systematic approach monthly:

- Gather documents: Current statement and corresponding accounting records

- Match transactions: Compare each statement line to recorded entries

- Identify discrepancies: Note missing transactions, amount differences, or duplicates

- Research variances: Investigate unmatched items

- Make adjustments: Correct accounting records as needed

- Document findings: Maintain reconciliation notes for audit trails

- Verify totals: Ensure ending balances match

Automated reconciliation becomes possible when statements are in spreadsheet format compatible with accounting software. Structured data enables matching algorithms to identify corresponding transactions across systems, flagging only items requiring manual review.

Understanding every component of your monthly credit card statement empowers better financial decision-making and helps identify opportunities to reduce costs, maximize rewards, and maintain accurate records. Whether managing personal finances or business accounts, systematic statement review prevents costly errors and provides valuable insights into spending patterns. Bank Statement Boss streamlines this process by converting PDF credit card statements into organized spreadsheets with 99% accuracy, compatible with major accounting platforms while maintaining bank-level security throughout the conversion process.