Understanding financial records is fundamental to running a successful business, yet many professionals struggle with the details of how transactions appear and are recorded. A statement transaction represents any individual financial activity documented on a bank or credit card statement, from deposits and withdrawals to fees and transfers. These documented activities form the backbone of financial tracking, tax preparation, and business analysis. As businesses increasingly rely on digital tools and automated systems, knowing how to read, interpret, and manage statement transactions has become more critical than ever.

What Is a Statement Transaction

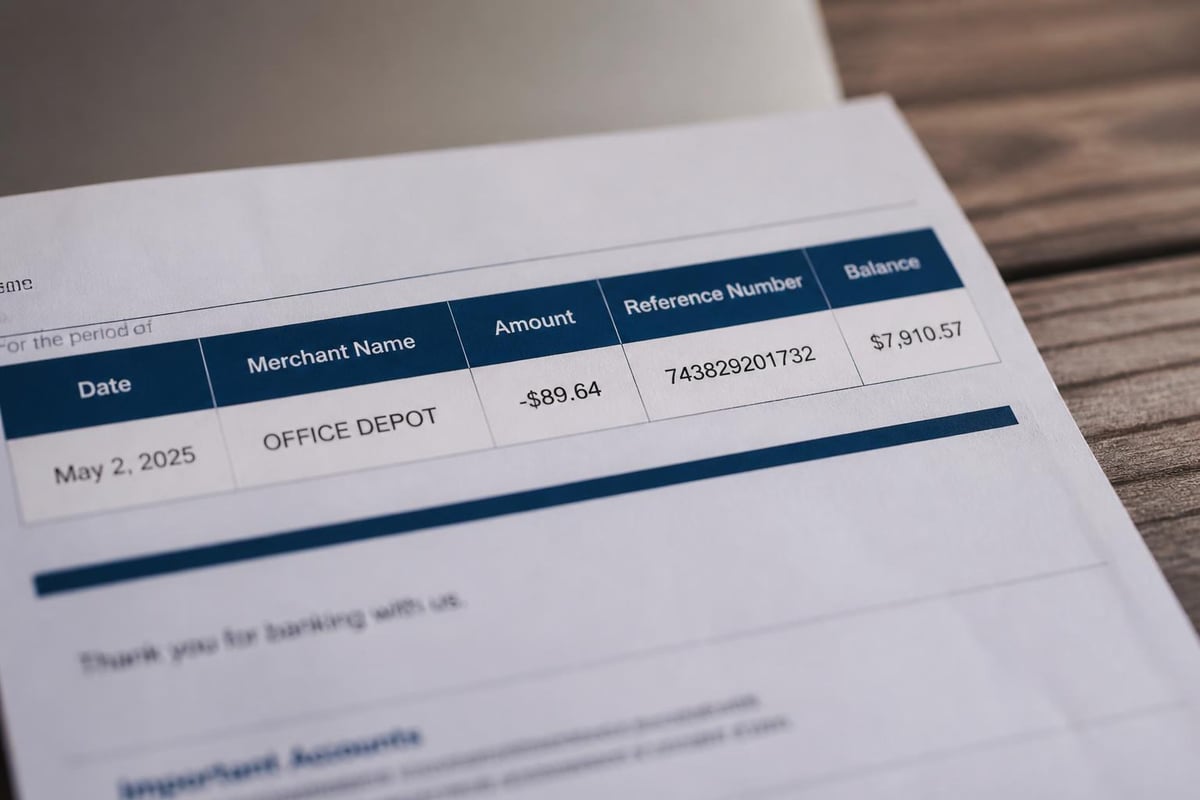

A statement transaction refers to any single entry recorded on a financial statement that reflects money moving into or out of an account. These transactions appear with specific details including the date, amount, description, and running balance. Financial institutions document every activity as a separate statement transaction to create a comprehensive record of account activity.

Core Components of Statement Transactions

Every statement transaction contains essential data points that help identify and categorize the activity. The transaction date indicates when the activity occurred, while the posting date shows when the bank processed it. The description field provides details about the merchant, transfer recipient, or transaction type.

Key elements include:

- Transaction date and time

- Merchant or payee name

- Transaction amount (debit or credit)

- Transaction reference number

- Category or transaction type

- Running account balance

The reference number serves as a unique identifier for each statement transaction, enabling businesses to track specific activities across multiple systems. This becomes particularly important when reconciling accounts or investigating discrepancies.

Types of Statement Transactions

Statement transactions fall into distinct categories based on their nature and purpose. Understanding these classifications helps businesses organize financial data and identify patterns in spending or revenue.

Debit Transactions

Debit transactions reduce the available balance in an account. These include purchases made with debit cards, ATM withdrawals, electronic fund transfers, and automatic bill payments. Each debit statement transaction removes funds from the account and appears as a negative entry on the statement.

Business expenses frequently generate debit transactions. When a company purchases supplies, pays vendors, or covers operational costs, each payment creates a distinct statement transaction. The format for bank details affects how these transactions appear and how easily they can be imported into accounting systems.

Credit Transactions

Credit transactions increase the account balance. Customer payments, wire transfers received, interest earned, and refunds all appear as credit statement transactions. These entries show positive amounts and contribute to the overall available funds.

| Transaction Type | Impact on Balance | Common Examples |

|---|---|---|

| Purchases | Decrease | Vendor payments, supplies, subscriptions |

| Deposits | Increase | Customer payments, transfers in |

| Fees | Decrease | Monthly fees, overdraft charges |

| Interest | Increase | Earned interest, rebates |

| Refunds | Increase | Returned items, reversed charges |

Pending vs. Posted Transactions

Not all statement transactions immediately affect the final balance. Pending transactions have been authorized but not yet cleared through the banking system. These appear separately from posted transactions, which have completed processing and permanently impact the account balance.

The distinction matters when reconciling accounts or analyzing cash flow. Businesses reviewing their checking statements must account for pending statement transactions that will settle in future periods.

How Statement Transactions Are Recorded

Financial institutions follow standardized processes for recording and displaying statement transactions. This consistency allows businesses to understand their financial activity regardless of which bank they use.

Digital Recording Systems

Modern banking relies on real-time digital systems that capture statement transactions instantaneously. When a card swipe occurs or an electronic transfer initiates, the banking network records the activity and generates a preliminary entry. This initial record may appear as pending before final settlement.

The processing payment phase involves multiple steps between authorization and final posting. During this period, the statement transaction exists in a temporary state while the banking network verifies funds, confirms authenticity, and completes the transfer between institutions.

Statement Generation

Banks compile all completed statement transactions into periodic statements, typically monthly. These documents provide a chronological record of every activity within the specified timeframe. Each statement transaction appears with complete details, creating an audit trail for the account holder.

Statement formats vary but generally include:

- Opening balance from the previous period

- Chronological list of all statement transactions

- Subtotals for debits and credits

- Fees and charges as separate entries

- Closing balance for the period

The generated statement serves as an official record that businesses use for accounting, tax preparation, and financial analysis. Converting these PDF statements into usable data formats has become essential for efficient bookkeeping.

Managing Statement Transactions for Business

Effective management of statement transactions directly impacts financial accuracy and operational efficiency. Businesses that establish robust processes for handling transaction data gain better visibility into their financial position.

Regular Reconciliation

Reconciling statement transactions against internal records prevents errors from compounding. This process involves comparing each entry on the bank statement with corresponding entries in accounting software. Discrepancies might indicate missing transactions, duplicate entries, or unauthorized activities.

Monthly reconciliation should become routine practice. Setting aside dedicated time to review every statement transaction ensures that financial records accurately reflect business activity. Some companies reconcile weekly or even daily for tighter financial control.

Categorizing Transactions

Proper categorization transforms raw statement transaction data into meaningful financial insights. Assigning categories like office supplies, marketing expenses, or client payments enables accurate reporting and tax preparation. Many accounting platforms offer automatic categorization, but manual review ensures accuracy.

Creating a consistent categorization system requires defining clear rules for different transaction types. A statement transaction from an office supply store should always map to the same expense category. This consistency improves reporting reliability and simplifies tax filing.

Digital Conversion and Integration

Converting PDF statements into spreadsheet format has become standard practice for businesses seeking efficiency. The PDF Bank Statement to Spreadsheet service enables companies to transform static documents into editable data that integrates with accounting platforms. This conversion preserves every statement transaction detail while making the information accessible for analysis.

Digital formats allow for filtering, sorting, and analyzing statement transactions in ways that paper statements cannot support. Businesses can quickly identify spending patterns, track specific vendors, or calculate category totals when transaction data exists in spreadsheet form.

Statement Transaction Accuracy and Verification

Maintaining accurate records requires vigilant oversight of statement transactions. Errors can occur at multiple points in the transaction lifecycle, from initial processing to final statement generation.

Common Errors

Statement transaction errors take various forms. Duplicate charges occur when a merchant processes the same payment twice. Incorrect amounts result from keying errors or system glitches. Missing transactions happen when activities fail to post properly.

Unauthorized transactions represent a more serious concern. These statement transactions appear without the account holder's knowledge or approval, potentially indicating fraud or identity theft. Regular statement review helps detect these issues quickly.

| Error Type | Cause | Resolution Method |

|---|---|---|

| Duplicate Charge | System error, merchant mistake | Contact merchant or bank |

| Wrong Amount | Processing error | Dispute with bank |

| Missing Transaction | System failure | Provide receipt, request investigation |

| Unauthorized Activity | Fraud, stolen credentials | Report immediately, freeze account |

Dispute Resolution

When errors appear in statement transactions, prompt action protects business finances. Most financial institutions provide specific procedures for disputing incorrect statement transactions. Businesses typically have 60 days from the statement date to report discrepancies.

Documentation strengthens dispute claims. Maintaining receipts, invoices, and correspondence related to each statement transaction provides evidence when challenging errors. Digital record-keeping makes retrieving this supporting documentation faster and more reliable.

Statement Transactions and Compliance

Regulatory requirements govern how businesses must maintain and report statement transaction records. Understanding these obligations helps companies avoid penalties and maintain good standing with authorities.

Record Retention Requirements

Tax authorities require businesses to retain statement transaction records for specific periods. In the United States, the IRS recommends keeping records for at least three years from the tax return filing date. Some situations require longer retention periods, particularly when dealing with employment taxes or property records.

Digital storage has simplified compliance with retention requirements. Scanning paper statements and maintaining electronic records of statement transactions creates easily accessible archives that meet regulatory standards. Many businesses now request statements in digital format from the outset to streamline their record-keeping.

Audit Preparation

During audits, examiners scrutinize statement transactions to verify reported income and expenses. Having organized, categorized transaction records demonstrates professionalism and expedites the audit process. Businesses with clear documentation of every statement transaction typically face fewer complications during examinations.

Preparation involves more than simply saving statements. Creating summaries, cross-referencing transactions with invoices, and maintaining supporting documentation for significant statement transactions helps auditors understand the business's financial activities.

Technology and Statement Transactions

Technological advancement has transformed how businesses interact with statement transactions. Automation, artificial intelligence, and cloud-based systems have replaced manual processes that once consumed significant time and resources.

Automated Transaction Import

Modern accounting software can automatically import statement transactions from financial institutions. This connectivity eliminates manual data entry and reduces transcription errors. Each statement transaction flows directly from the bank into the accounting system, where rules-based categorization applies appropriate classifications.

The automation extends beyond simple imports. Advanced systems can match statement transactions with outstanding invoices, flag unusual activities, and generate real-time financial reports. This capability gives businesses unprecedented visibility into their financial position.

AI-Powered Processing

Artificial intelligence has revolutionized statement transaction processing. Machine learning algorithms can identify patterns, categorize transactions with increasing accuracy, and detect anomalies that might indicate errors or fraud. These systems learn from corrections and adjustments, continuously improving their performance.

AI technology enables the conversion of PDF statements into structured data with remarkable precision. By recognizing statement transaction patterns and extracting relevant information, these systems transform unusable documents into actionable financial data.

Security Considerations

Digital handling of statement transactions introduces security requirements. Businesses must protect sensitive financial data from unauthorized access, theft, or loss. Encryption, secure storage, and access controls form the foundation of transaction data security.

Bank-level security protocols have become the standard for services handling statement transaction data. Companies providing statement conversion or financial management tools implement multiple layers of protection to safeguard client information. When selecting tools or services, businesses should verify security certifications and data handling practices.

Best Practices for Statement Transaction Management

Implementing structured processes for managing statement transactions improves accuracy and efficiency while reducing the risk of errors or oversights.

Establish these fundamental practices:

- Review statements within three business days of receipt

- Reconcile all statement transactions monthly at minimum

- Maintain a consistent categorization system

- Document unusual or large transactions immediately

- Store digital copies with secure backup systems

- Set up alerts for large or unusual statement transactions

- Train staff on proper transaction handling procedures

Regular training ensures that everyone involved in financial management understands how to handle statement transactions correctly. This includes recognizing different transaction types, knowing when to escalate concerns, and following established procedures for categorization and documentation.

Creating a Transaction Review Workflow

A systematic review workflow prevents statement transactions from being overlooked. Designating specific team members to handle different aspects of transaction management creates accountability. One person might handle initial categorization, while another performs reconciliation, and a supervisor approves unusual entries.

The workflow should include checkpoints for verifying accuracy. Before closing monthly books, a final review of all statement transactions catches any remaining discrepancies. This multi-layered approach significantly reduces the likelihood of errors persisting into financial reports.

Statement Transactions Across Multiple Accounts

Businesses operating multiple bank accounts face additional complexity in managing statement transactions. Each account generates its own statement with distinct transaction histories that must be tracked, reconciled, and consolidated for comprehensive financial reporting.

Consolidated Reporting

Creating unified financial views requires aggregating statement transactions from all accounts. This consolidation reveals the complete financial picture, including total cash flow, combined expenses, and overall financial position. Without proper consolidation, businesses may miss important trends or make decisions based on incomplete information.

Cross-account transfers require particular attention. These appear as statement transactions in both accounts - a debit in one and a credit in another. Proper handling prevents double-counting and ensures accurate financial reporting.

Multi-Account Reconciliation

Reconciling multiple accounts demands organization and attention to detail. Businesses often find that maintaining separate records for each account while also creating consolidated views provides the best balance. This approach allows for account-specific analysis while supporting overall financial oversight.

Using standardized processes across all accounts streamlines reconciliation efforts. When the same categorization rules, verification procedures, and documentation standards apply to every statement transaction regardless of account, the process becomes more efficient and less error-prone.

Managing statement transactions effectively forms the foundation of sound financial management for any business. Understanding transaction types, implementing robust tracking systems, and maintaining accurate records enables better decision-making and ensures compliance with regulatory requirements. As financial processes become increasingly digital, businesses that adopt modern tools for handling statement transaction data gain significant competitive advantages. Bank Statement Boss helps companies transform their PDF statements into organized, actionable data with AI-powered accuracy, making transaction management faster and more reliable while maintaining the security your financial information demands.