Understanding my credit statement is a fundamental skill for maintaining financial health and avoiding costly mistakes. Every month, credit card issuers send detailed statements that contain vital information about spending patterns, payment obligations, and account status. However, many cardholders simply glance at the minimum payment due and miss critical details that could impact their credit score, budget, and long-term financial goals. This comprehensive guide breaks down every section of my credit statement to help you make informed decisions and take control of your finances.

Essential Components of My Credit Statement

Every credit statement follows a similar structure, though the exact layout varies by issuer. Understanding how to read your credit card statement begins with identifying the primary sections that appear on every statement.

Account Summary Section

The account summary provides a snapshot of your financial position for the billing cycle. This section displays your previous balance, new charges, payments received, credits applied, and the current balance. The previous balance represents what you owed at the end of the last billing cycle, while the new balance shows your total obligation for the current period.

Key figures in this section include:

- Previous Balance: Outstanding amount from last statement

- Payments and Credits: Total reductions to your balance

- Purchases and Adjustments: New charges added during the cycle

- Cash Advances: Money borrowed against your credit line

- Fees Charged: Penalty fees, annual fees, or other charges

- Interest Charged: Finance charges on unpaid balances

The account summary also shows your credit limit and available credit, helping you monitor your credit utilization ratio, which significantly impacts your credit score.

Payment Information and Due Dates

One of the most critical sections of my credit statement is the payment information area. This section prominently displays the payment due date, minimum payment amount, and often includes a warning about the consequences of making only minimum payments.

The minimum payment is calculated based on your balance, typically ranging from 1% to 3% of the total balance plus interest and fees. Making only the minimum payment extends your repayment timeline significantly and increases the total interest paid over time.

| Payment Scenario | Amount | Time to Pay Off | Total Interest |

|---|---|---|---|

| Minimum Payment Only | 2% of balance | 15-30 years | 150-300% of principal |

| Fixed $100/month | $100 | 2-5 years | 20-50% of principal |

| Full Balance | Full amount | 1 month | $0 |

Understanding these payment dynamics helps you make strategic decisions about how to manage your credit card obligations effectively.

Transaction Details and Activity Records

The transaction section of my credit statement lists every purchase, payment, fee, and credit processed during the billing cycle. This detailed record serves multiple purposes beyond simple record-keeping.

Reviewing Transaction History

Each transaction entry typically includes the transaction date, posting date, merchant name, and amount. The transaction date is when you made the purchase, while the posting date is when the charge was officially processed by your card issuer.

Carefully reviewing this section helps you:

- Identify unauthorized charges or fraudulent activity

- Track spending patterns across different categories

- Verify purchase amounts match receipts

- Catch merchant errors or duplicate charges

- Monitor subscription services and recurring payments

Many cardholders find converting their statements to digital formats helpful for analysis. Services that convert PDF bank statements to usable spreadsheets make it easier to categorize transactions, create budgets, and integrate financial data with accounting software.

Understanding Transaction Categories

Modern credit statements often categorize transactions by spending type, such as dining, travel, groceries, or gas. This categorization provides insights into spending habits and helps identify areas where you might reduce expenses.

Some issuers provide year-to-date spending summaries by category, making it easier to track annual budgets and prepare for tax season. Business owners particularly benefit from these categorizations when separating personal and business expenses.

Interest Charges and APR Calculations

The interest and fees section of my credit statement explains how finance charges are calculated and applied. Understanding credit card interest is essential for minimizing costs and managing debt effectively.

Annual Percentage Rate Breakdown

Your statement lists different APRs for various transaction types. Purchase APR applies to regular purchases, while cash advance APR is typically higher and begins accumulating interest immediately without a grace period. Balance transfer APR may offer promotional rates for transferred balances.

The statement shows how your APR is calculated using the daily periodic rate multiplied by your average daily balance. This method means interest compounds daily, making even small balances costly if carried over multiple months.

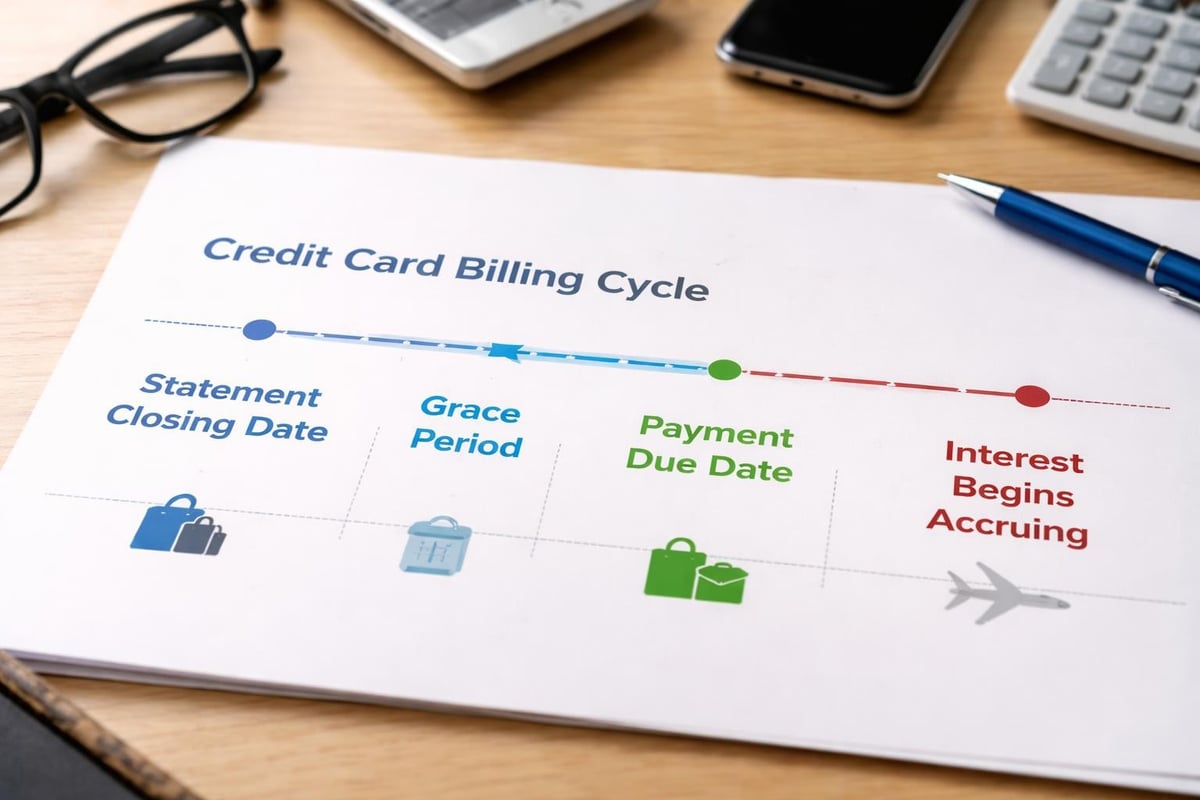

Grace Periods and Interest Avoidance

Most credit cards offer a grace period of 21 to 25 days between the statement closing date and payment due date. During this period, no interest accrues on new purchases if you paid the previous balance in full. Understanding this timing helps you avoid unnecessary interest charges.

Fees, Penalties, and Additional Charges

My credit statement itemizes all fees assessed during the billing cycle. These charges can significantly impact your overall costs and should be reviewed carefully each month.

Common Fee Types

Late payment fees are assessed when payments arrive after the due date, typically ranging from $25 to $40 depending on your payment history. Over-limit fees apply if you exceed your credit limit, though many issuers have eliminated these charges.

Foreign transaction fees of 1% to 3% apply to purchases made in foreign currencies or through international merchants. Cash advance fees usually equal 3% to 5% of the advance amount, plus immediate interest charges.

Understanding these fees helps you avoid unnecessary costs. Detailed breakdowns of credit card fees enable better financial planning and informed decision-making about card usage.

Rewards, Points, and Benefits Summary

For rewards credit cards, my credit statement includes a section detailing points earned, redeemed, and available. This summary shows your rewards balance and may highlight upcoming expiration dates or bonus opportunities.

Tracking Rewards Effectively

The rewards summary typically breaks down points by category:

- Points earned from base spending

- Bonus points from special categories

- Points from promotional offers

- Points redeemed during the cycle

- Total points available

Some statements include the estimated cash value of your rewards or provide redemption options directly on the statement. Monitoring this section ensures you maximize benefits and redeem points before expiration.

Account Changes and Important Notices

The notices section of my credit statement communicates policy changes, rate adjustments, or important account information. Federal regulations require issuers to provide 45 days' notice before implementing significant changes to terms and conditions.

Regulatory Information and Consumer Rights

Your statement includes information about your rights regarding credit card statements, including dispute procedures, billing error resolution, and fraud protection. The Fair Credit Billing Act requires specific disclosures about how to report billing errors within 60 days of the statement date.

This section also contains contact information for customer service, fraud reporting, and account inquiries. Keeping this information accessible ensures you can quickly address issues when they arise.

Digital Statement Management and Security

As financial management becomes increasingly digital, understanding how to securely access and manage my credit statement online is essential. Electronic statements offer convenience and enhanced security features compared to paper statements.

Benefits of Digital Statement Access

Online statement access provides several advantages:

- Immediate availability on the statement closing date

- Searchable transaction history across multiple billing cycles

- Easy export options for financial software integration

- Reduced identity theft risk from mail interception

- Environmental benefits from reduced paper usage

However, digital statements require proper security measures. Always access your account through official channels, enable two-factor authentication, and verify the security protocols of any third-party services you use for financial management.

Converting Statements for Analysis

Many financial professionals and business owners need to convert my credit statement from PDF format into analyzable data. This conversion enables detailed expense tracking, tax preparation, and integration with accounting software like QuickBooks or Xero.

Modern AI-powered conversion services maintain data accuracy while transforming static PDF statements into dynamic spreadsheets. This technology recognizes transaction patterns, categorizes expenses automatically, and preserves the integrity of financial data throughout the conversion process.

Monitoring Credit Utilization and Financial Health

My credit statement provides critical information for monitoring your overall financial health. The relationship between your current balance and credit limit, known as credit utilization, significantly impacts your credit score.

Optimal Utilization Strategies

Credit scoring models favor utilization ratios below 30%, with ratios under 10% considered excellent. Your statement shows both your credit limit and current balance, making it easy to calculate this important metric.

| Utilization Rate | Credit Score Impact | Recommended Action |

|---|---|---|

| Under 10% | Excellent | Maintain current habits |

| 10-30% | Good | Monitor spending carefully |

| 30-50% | Moderate negative | Pay down balance |

| 50-70% | Significant negative | Prioritize debt reduction |

| Over 70% | Severe negative | Urgent debt management needed |

Recent guidance on reading credit statements emphasizes monitoring utilization across all reporting periods, not just the statement closing date, since some issuers report to credit bureaus multiple times per month.

Statement Cycles and Timing Considerations

Understanding the timing of my credit statement helps optimize payment strategies and maximize interest-free periods. The statement cycle typically runs for 30 or 31 days, closing on the same date each month.

Strategic Payment Timing

The statement closing date determines which transactions appear on the current statement versus the next one. Making large purchases just after the closing date gives you the maximum grace period before payment is due.

Some cardholders make multiple payments throughout the month to keep their reported balance low, even if they pay in full each month. This strategy can improve credit scores by reducing the utilization rate reported to credit bureaus.

Dispute Resolution and Error Correction

My credit statement includes procedures for disputing charges and reporting billing errors. Federal law provides strong consumer protections, but you must act within specified timeframes.

Filing a Billing Dispute

To dispute a charge, you must submit a written notice within 60 days of the statement date. Your notice should include your name, account number, the disputed amount, and a detailed explanation of why you believe the charge is incorrect.

The issuer must acknowledge your dispute within 30 days and resolve it within two billing cycles (not exceeding 90 days). During the investigation, you are not required to pay the disputed amount, and the issuer cannot report it as delinquent.

Business Credit Statement Considerations

For business credit cards, my credit statement includes additional considerations relevant to company finances. Business statements often provide enhanced reporting features, expense categorization by employee or department, and integration options with corporate accounting systems.

Employee Card Management

Business statements consolidate charges from multiple employee cards, showing individual spending alongside total company expenditures. This transparency helps businesses monitor spending patterns, enforce policy compliance, and identify cost-saving opportunities.

Detailed transaction data from business credit statements supports tax preparation, client billing, and budget planning. Converting these statements into structured spreadsheet formats streamlines accounting processes and ensures accurate record-keeping for audit purposes.

Understanding every component of my credit statement empowers better financial decision-making, helps avoid costly fees, and supports long-term credit health. From transaction verification to interest calculation, each section provides valuable insights into your spending patterns and account status. For business owners and financial professionals who need to analyze credit statement data in depth, Bank Statement Boss uses AI technology to convert PDF credit card statements into spreadsheets with 99% accuracy, offering bank-level security and compatibility with major accounting platforms to streamline your financial management processes.