A monthly statement serves as a comprehensive record of all financial activity within your account over a 30-day period. Whether you're managing personal finances or running a business, understanding the components and purpose of these documents is essential for maintaining accurate financial records, detecting fraud, and ensuring proper reconciliation with your accounting systems. This financial snapshot arrives regularly from banks, credit unions, credit card companies, and other financial institutions, providing a detailed overview that helps you stay informed about your money.

Understanding What a Monthly Statement Contains

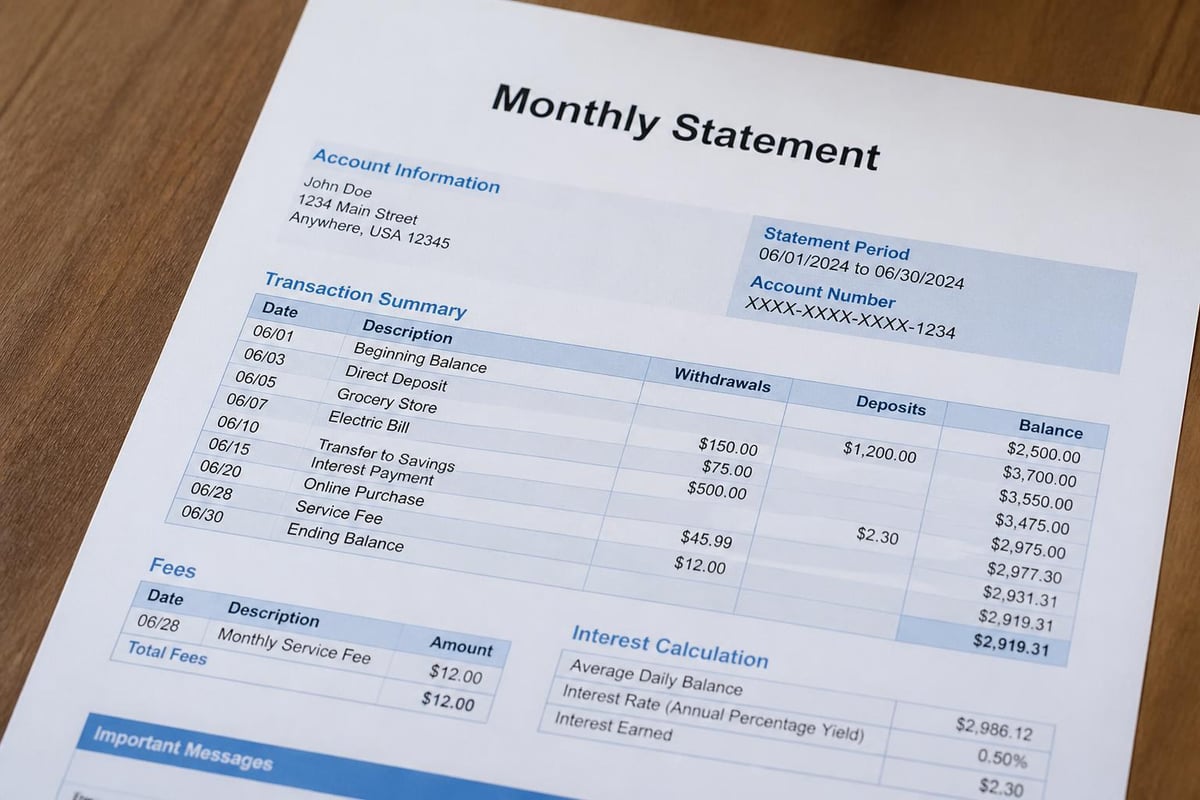

Every monthly statement follows a standard structure designed to provide complete transparency about your account activity. The document typically begins with account holder information, including your name, address, and account number, followed by the statement period dates.

The most critical component is the transaction history, which lists every deposit, withdrawal, payment, and fee chronologically. This section shows the date of each transaction, a description of the activity, and the amount debited or credited to your account.

Key Components Found in Every Statement

Your monthly statement includes several essential elements that work together to provide a complete financial picture:

- Beginning and ending balance: Shows your account status at the start and end of the statement period

- Transaction details: Complete list of all account activity with dates and descriptions

- Interest earned or charged: Applicable rates and calculations for the period

- Fees and service charges: Any costs associated with maintaining or using the account

- Year-to-date summaries: Cumulative totals for certain categories like interest or fees

Federal regulations often dictate what information must appear on these documents. According to federal banking regulations, financial institutions must provide monthly statements for accounts that experience electronic fund transfers during that period.

The level of detail varies by institution and account type. Business accounts typically provide more granular transaction descriptions, merchant category codes, and enhanced reporting features that support accounting reconciliation processes.

Regulatory Requirements for Monthly Statements

Financial institutions operate under strict regulatory frameworks that mandate when and how they must provide account statements to customers. These requirements exist to protect consumers and ensure transparency in financial transactions.

For checking accounts, federal regulations require monthly statements when electronic fund transfers occur during the statement period. This includes ATM withdrawals, debit card purchases, direct deposits, and automated bill payments.

Statement Frequency by Account Type

Different account types follow distinct statement schedules based on activity levels and regulatory requirements:

| Account Type | Statement Frequency | Regulatory Trigger |

|---|---|---|

| Checking with EFT activity | Monthly | Electronic transactions occurred |

| Savings with EFT activity | Monthly | Electronic transactions occurred |

| Inactive checking/savings | Quarterly | No electronic activity |

| Credit cards | Monthly | Account has balance or activity |

| Mortgage accounts | Monthly | Required by periodic statement rule |

The periodic statement rule for mortgages mandates specific disclosures that help homeowners understand their loan status, payment application, and outstanding balance.

For specialized accounts like retail forex trading, institutions must provide monthly statements detailing open positions, unrealized profits or losses, and margin requirements. These regulatory requirements ensure customers have complete visibility into their financial positions.

How Businesses Use Monthly Statements

Business owners rely on monthly statements for multiple critical functions that go far beyond simple account monitoring. These documents form the foundation of accurate bookkeeping, tax preparation, and financial analysis.

Reconciliation represents the primary use case for most businesses. This process involves matching statement transactions against internal accounting records to identify discrepancies, catch errors, and ensure every dollar is properly accounted for.

Essential Business Applications

Cash flow management becomes significantly easier when you regularly review monthly statements. By analyzing deposit patterns and payment timing, businesses can predict future cash positions and avoid overdrafts or missed payment opportunities.

Expense tracking and categorization relies heavily on statement data. Businesses must classify transactions by type-supplies, payroll, utilities, travel-to understand spending patterns and prepare accurate financial reports.

Tax preparation and audit support requires comprehensive transaction records. Monthly statements provide the documentation needed to substantiate deductions, verify income, and respond to inquiries from tax authorities or auditors.

Many businesses need to convert their PDF statements into spreadsheet formats for easier analysis and integration with accounting systems. Services that convert PDF bank statements to usable spreadsheets help streamline this process, making reconciliation faster and more accurate.

Digital vs. Paper Statement Delivery

The transition from paper to digital statements has transformed how individuals and businesses access their financial information. Each delivery method offers distinct advantages and considerations worth understanding.

Paper statements arrive by mail and provide a tangible record that some people find easier to file and reference. They don't require internet access to review and can serve as immediate proof of account status for various purposes.

Digital statements, also known as e-statements, offer immediate availability through online banking portals or email delivery. These electronic versions typically become available several days before paper versions would arrive by mail.

Comparing Statement Delivery Options

| Feature | Paper Statements | Digital Statements |

|---|---|---|

| Delivery speed | 5-10 business days | Instant access |

| Storage | Physical filing required | Cloud-based or download |

| Search capability | Manual review only | Keyword searchable |

| Environmental impact | Paper consumption | Minimal footprint |

| Cost to institution | Higher (printing, postage) | Lower (electronic delivery) |

| Security risk | Mail theft possible | Account access dependent |

Most financial institutions now encourage digital adoption by offering paperless incentives or charging fees for paper statement delivery. The shift toward digital has created new challenges around document management and data extraction, particularly for businesses that need transaction data in spreadsheet format for accounting purposes.

Statement Review Best Practices

Regularly reviewing your monthly statement protects against fraud, identifies billing errors, and maintains accurate financial records. Establishing a consistent review process helps catch problems early when they're easier to resolve.

Start by verifying the beginning balance matches your previous statement's ending balance. Any discrepancy signals either an error or unrecorded transaction that needs investigation.

Step-by-Step Review Process

- Compare beginning and ending balances against your personal records to identify major discrepancies

- Review all transactions chronologically and mark each one you recognize as legitimate

- Flag unfamiliar transactions for immediate investigation and potential fraud reporting

- Verify interest calculations and fees match your account agreement and expectations

- Check deposit timing to ensure all expected payments arrived and were properly credited

- Document any discrepancies with dates, amounts, and descriptions for follow-up

- Update your accounting records to reflect any corrections or missed entries

When reviewing credit card statements specifically, pay special attention to recurring charges that may have increased, trial subscriptions that converted to paid memberships, or duplicate charges from the same merchant.

Business owners should cross-reference checking statements against accounts payable and receivable records to ensure all expected transactions cleared properly. This reconciliation process becomes significantly easier with organized, searchable transaction data.

Common Monthly Statement Issues and Solutions

Even with careful account management, problems occasionally arise with monthly statements. Understanding common issues helps you address them quickly and effectively.

Missing transactions represent one of the most frequent concerns. Deposits or payments that should appear on your statement but don't require immediate attention, as they may indicate processing delays, technical errors, or failed transactions.

Unauthorized charges demand urgent action. Federal law limits your liability for fraudulent transactions, but protection depends on how quickly you report suspicious activity. Review statements within 60 days to maintain full protections under the law.

Addressing Statement Discrepancies

Timing differences often cause apparent discrepancies between your records and your monthly statement. Checks written near month-end may not clear until the following statement period, and deposits made after business hours might post the next day.

Fee surprises occur when account holders aren't familiar with their fee schedules. Common charges include:

- Monthly maintenance fees for accounts below minimum balance requirements

- Overdraft or insufficient funds fees when payments exceed available funds

- ATM fees for using out-of-network machines

- Wire transfer fees for sending or receiving funds electronically

- Paper statement fees if you haven't opted for electronic delivery

When you identify legitimate errors, contact your financial institution immediately. Most banks provide specific timeframes for disputing transactions or reporting errors, and delays can limit your recourse options.

Statement Retention and Organization

Proper storage and organization of monthly statements serves multiple purposes, from tax preparation to loan applications. Determining how long to keep these documents depends on their purpose and your specific circumstances.

Tax-related statements should be retained for at least seven years, as the IRS can audit returns up to six years after filing in cases involving substantial underreporting. Many financial advisors recommend keeping supporting documents for the same period.

Retention Guidelines by Document Type

Different statement types warrant different retention periods based on their potential future utility:

- Regular checking/savings statements: Keep for one year unless needed for tax purposes

- Statements showing tax-deductible transactions: Retain for seven years minimum

- Year-end summary statements: Keep permanently with tax returns

- Mortgage statements: Maintain until loan payoff plus seven years

- Investment and retirement account statements: Hold until account closure plus seven years

- Credit card statements: Keep for one year; longer if business-related

Digital organization offers advantages over paper filing systems. Scanning paper statements or downloading e-statements creates searchable archives that occupy minimal physical space. However, ensuring proper backup procedures protect against data loss.

Understanding the definition and types of account statements helps you categorize documents appropriately and develop retention policies that meet both regulatory requirements and practical needs.

Leveraging Technology for Statement Management

Modern technology has revolutionized how businesses and individuals handle monthly statement data. Automated solutions reduce manual data entry, improve accuracy, and free up time for higher-value financial activities.

Optical character recognition (OCR) technology can extract transaction data from PDF statements, though accuracy varies significantly based on document quality and formatting consistency. Manual verification often remains necessary to catch extraction errors.

Application programming interfaces (APIs) offered by many financial institutions enable direct data feeds into accounting software, eliminating the need for manual statement processing entirely. However, API access typically requires specific account types and may involve additional fees.

Spreadsheet conversion tools address the gap between PDF statements and accounting software. By transforming statement data into structured formats, these solutions enable easier sorting, filtering, and analysis of transaction information.

When selecting technology solutions for statement management, consider these factors:

- Accuracy rates for data extraction and conversion

- Security measures protecting sensitive financial information during processing

- Integration capabilities with existing accounting platforms and workflows

- Processing speed for handling multiple statements or large transaction volumes

- Cost structure relative to time savings and error reduction benefits

Banks and credit unions vary in how often they provide statements and what formats they support. Understanding these patterns helps you choose tools and processes that align with your institution's capabilities.

Statement Analysis for Financial Health

Beyond simple reconciliation, monthly statements provide valuable insights into spending patterns, financial habits, and opportunities for improvement. Regular analysis transforms these documents from compliance requirements into strategic financial tools.

Trend identification emerges when you compare multiple months of statement data. Increasing average daily balances might indicate improved cash flow, while growing fee totals could signal account structure problems or behavior changes worth addressing.

Expense categorization reveals where money actually goes versus where you think it goes. Many people discover surprising patterns when they classify every transaction over several months-perhaps more spending on subscriptions than anticipated or seasonal variations in certain expense categories.

For businesses, statement analysis supports budgeting and forecasting. Historical transaction patterns inform realistic projections for future periods, helping companies plan for seasonal variations, anticipate cash needs, and identify cost reduction opportunities.

Key Metrics to Track Monthly

Monitor these indicators across multiple statement periods to understand your financial trajectory:

- Average daily balance and month-over-month changes

- Total deposits and income sources with growth trends

- Total withdrawals and major expense categories

- Frequency and amount of fees paid

- Number of overdrafts or low balance occurrences

- Interest earned on deposit accounts or paid on credit lines

Creating a dashboard that tracks these metrics over time provides perspective that individual monthly statements cannot offer. Spreadsheet tools enable this analysis, which is why many businesses prioritize converting PDF statements into workable data formats.

Understanding and effectively utilizing your monthly statement provides the foundation for sound financial management and accurate record-keeping. By implementing consistent review processes, leveraging appropriate technology, and analyzing statement data for insights, you transform these routine documents into strategic financial tools. Bank Statement Boss helps businesses streamline statement processing by converting PDF bank and credit card statements into accurate spreadsheets compatible with major accounting platforms, reducing manual data entry while maintaining bank-level security for your sensitive financial information.