The financial foundation of every banking institution rests on rigorous accounting practices that govern how deposits, loans, and investments are recorded and reported. Accounting in bank operations differs significantly from traditional business accounting due to unique regulatory requirements, complex financial instruments, and the critical role banks play in the broader economy. Understanding these specialized practices is essential for anyone working with financial data in the banking sector.

The Unique Framework of Bank Accounting

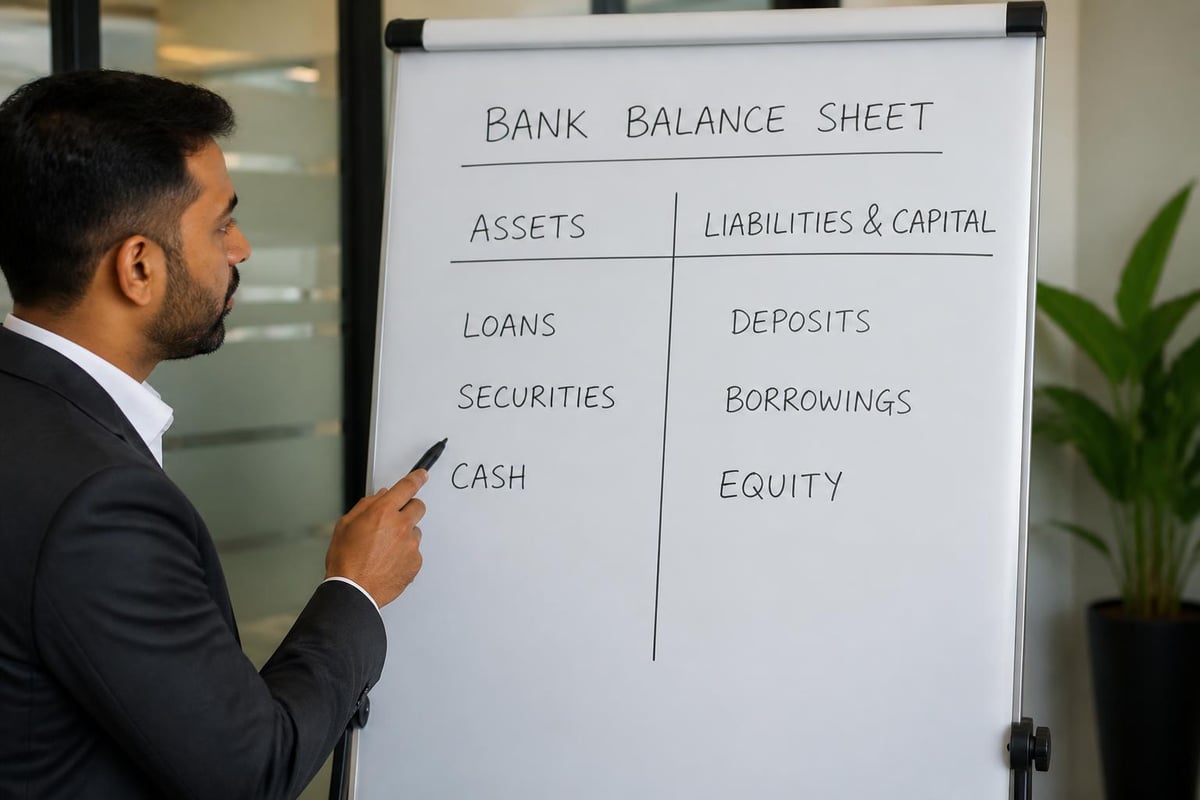

Banking institutions operate under a distinct accounting framework that reflects their role as financial intermediaries. Unlike retail or manufacturing businesses where inventory and cost of goods sold dominate the balance sheet, accounting in bank settings focuses primarily on financial assets and liabilities.

Assets and Liabilities in Banking Context

The asset structure in banking reverses what most people consider typical business operations. Loans extended to customers represent the primary asset category, while customer deposits constitute the main liability. This inverse relationship stems from the fundamental business model where banks borrow money (through deposits) to lend it out at higher interest rates.

Key asset categories include:

- Cash and cash equivalents

- Securities and investment portfolios

- Loan portfolios (commercial, consumer, mortgage)

- Physical property and equipment

- Intangible assets including goodwill

Primary liability categories encompass:

- Demand deposits and savings accounts

- Time deposits and certificates of deposit

- Borrowings from other financial institutions

- Subordinated debt instruments

- Federal funds purchased

The Federal Deposit Insurance Corporation's accounting guidance emphasizes the critical importance of accurate classification and measurement of these financial instruments to ensure regulatory compliance and proper risk assessment.

Regulatory Standards Governing Bank Accounting

Federal regulations establish strict accounting requirements that banking institutions must follow. Title 12 U.S. Code § 1831n mandates that insured depository institutions maintain books and records in accordance with generally accepted accounting principles (GAAP) and file consolidated reports of condition and income.

Compliance with GAAP and Regulatory Requirements

Under 12 CFR § 162.1, federal savings associations must adhere to U.S. GAAP and related disclosure standards unless statutory or regulatory provisions specify otherwise. This dual framework creates unique challenges for accounting professionals in banking.

| Regulatory Body | Primary Focus | Key Requirements |

|---|---|---|

| OCC | National banks and federal savings associations | Accounting interpretations and supervisory guidance |

| FDIC | Insured depository institutions | Credit loss allowances and financial reporting |

| Federal Reserve | Bank holding companies | Consolidated financial statements and capital adequacy |

| SEC | Publicly traded banks | Public disclosure and investor protection |

The Office of the Comptroller of the Currency's Bank Accounting Advisory Series provides interpretations that promote consistent application of accounting standards across national banks and federal savings associations.

Revenue Recognition in Banking Operations

Revenue recognition for accounting in bank environments involves several distinct income streams, each with specific recognition criteria and timing considerations.

Interest Income and Expense

Net interest income represents the difference between interest earned on assets (primarily loans and securities) and interest paid on liabilities (deposits and borrowings). Banks recognize interest income using the accrual method, recording it as it is earned rather than when cash is received.

Interest income recognition follows these principles:

- Calculate daily accruals based on outstanding principal balances

- Apply the contractual interest rate to determine periodic income

- Suspend accrual on non-performing loans meeting specific criteria

- Record recovered interest on previously charged-off loans as current income

Interest expense calculation mirrors this approach, with daily accruals on deposit accounts, borrowed funds, and debt instruments. The resulting net interest margin serves as a critical profitability indicator for banking operations.

Non-Interest Income Sources

Modern banks derive substantial revenue from fee-based services. These income streams require careful evaluation to determine proper recognition timing under GAAP standards.

Non-interest income categories typically include:

- Service charges on deposit accounts

- Loan origination and servicing fees

- Investment advisory and wealth management fees

- Interchange fees from payment card transactions

- Gains or losses on securities sales

When working with bank statement formats that detail these transactions, accounting teams must correctly classify each revenue type to ensure accurate financial reporting and regulatory compliance.

Loan Loss Provisioning and Allowance Estimation

One of the most critical aspects of accounting in bank operations involves estimating and maintaining adequate allowances for credit losses. This process requires significant judgment and sophisticated modeling techniques.

Current Expected Credit Loss (CECL) Model

Since 2023, banks have implemented the CECL accounting standard, which fundamentally changed how institutions estimate credit losses. Rather than waiting for probable losses to occur, CECL requires banks to estimate expected losses over the life of loans at origination.

The implementation involves these critical steps:

- Data gathering: Collect historical loss data, current loan characteristics, and economic forecasts

- Segmentation: Group loans by similar risk characteristics

- Loss rate estimation: Calculate expected default frequencies and loss given default

- Reasonable and supportable forecasting: Project economic conditions affecting credit quality

- Qualitative adjustments: Incorporate factors not captured in quantitative models

This forward-looking approach significantly impacts how accounting in bank statements reflects loan portfolio quality and creates greater volatility in earnings during economic cycles.

Financial Statement Preparation and Reporting

Banking institutions prepare comprehensive financial statements that provide transparency into their financial condition and operating performance. These statements follow specific formats tailored to banking operations.

The Call Report Structure

National banks file quarterly Consolidated Reports of Condition and Income, commonly known as Call Reports. These detailed filings contain extensive schedules covering:

| Schedule | Content Area | Purpose |

|---|---|---|

| RC | Balance Sheet | Report assets, liabilities, and equity |

| RI | Income Statement | Detail revenue, expenses, and net income |

| RC-B | Securities | Disclose investment portfolio composition |

| RC-C | Loans and Leases | Break down loan portfolio by category |

| RC-R | Regulatory Capital | Calculate capital ratios for adequacy |

The granular detail required in Call Reports exceeds typical corporate financial reporting, reflecting the heightened regulatory scrutiny of banking institutions.

Internal Management Reporting

Beyond regulatory filings, accounting in bank management relies on internal reports that provide real-time insights into operational performance. These reports often require data from multiple sources, including transaction systems, loan platforms, and core banking applications.

Modern accounting teams increasingly leverage technology to consolidate this information efficiently. Services that convert PDF bank statements to spreadsheets enable faster analysis and reconciliation by transforming static documents into workable data formats compatible with accounting platforms.

Asset and Liability Management Accounting

Effective asset-liability management (ALM) requires sophisticated accounting techniques to measure interest rate risk, liquidity risk, and market risk exposures.

Interest Rate Risk Measurement

Banks use various methods to quantify how interest rate changes affect net interest income and economic value of equity:

- Gap analysis: Measures the difference between rate-sensitive assets and liabilities in specific time periods

- Duration analysis: Calculates the weighted average time to receive cash flows, indicating price sensitivity to rate changes

- Simulation modeling: Projects net interest income under various rate scenarios

These measurements inform strategic decisions about loan pricing, deposit rates, and investment portfolio composition.

Liquidity Accounting and Monitoring

Maintaining adequate liquidity represents a fundamental safety and soundness concern. Accounting principles and practices in banking require continuous monitoring of liquid assets relative to potential funding needs.

Key liquidity metrics include:

- Loan-to-deposit ratio

- Available borrowing capacity at Federal Home Loan Banks

- Unencumbered securities available for repo transactions

- Estimated uninsured deposit volatility

Deposit Accounting Complexity

While deposits appear straightforward, accounting in bank settings reveals significant complexity in tracking and reporting various deposit types.

Transaction Processing and Daily Reconciliation

Banks process millions of transactions daily across checking accounts, savings accounts, and money market deposits. Each transaction requires proper posting, interest calculation, and fee assessment.

The reconciliation process involves:

- Matching internal transaction records to Federal Reserve settlement data

- Identifying and resolving discrepancies between subsidiary ledgers and general ledger

- Confirming automated clearing house (ACH) transactions settled correctly

- Verifying wire transfer debits and credits

- Reconciling ATM and debit card transactions

Understanding checking statements and their underlying accounting entries helps ensure accuracy in this daily reconciliation process.

Interest Calculation Methodologies

Different deposit products use varying interest calculation methods, creating accounting complexity:

| Product Type | Calculation Method | Accrual Frequency |

|---|---|---|

| Savings accounts | Daily balance method | Monthly |

| Money market deposits | Tiered rate structure | Monthly |

| Certificates of deposit | Simple or compound interest | At maturity or periodic |

| Checking accounts | Minimum balance or average balance | Monthly |

Accurate interest accrual accounting ensures customers receive correct compensation while the bank properly expenses interest costs.

Investment Securities Accounting

Banking investment portfolios require careful accounting treatment based on management intent and the characteristics of each security.

Classification Categories

GAAP requires banks to classify investment securities into three categories with different accounting treatments:

Held-to-maturity (HTM): Debt securities the bank has positive intent and ability to hold until maturity, carried at amortized cost.

Available-for-sale (AFS): Debt and equity securities not classified as trading or HTM, carried at fair value with unrealized gains and losses reported in other comprehensive income.

Trading securities: Securities bought principally for short-term profit, carried at fair value with unrealized gains and losses flowing through current earnings.

The classification decision significantly impacts reported earnings volatility and balance sheet presentation, making it a critical judgment in accounting in bank portfolios.

Impairment Assessment

Bank accountants must regularly assess whether declines in security values represent credit losses requiring recognition through earnings or temporary market fluctuations. This evaluation considers:

- Extent and duration of fair value decline below amortized cost

- Financial condition and near-term prospects of the issuer

- Intent and ability to hold the security until recovery

- Structure and credit enhancement features of the security

Technology and Automation in Bank Accounting

Modern banking accounting increasingly relies on technology to handle the volume and complexity of financial transactions while meeting stringent regulatory deadlines.

Automated Reconciliation Systems

Advanced reconciliation platforms automatically match thousands of transactions daily, flagging exceptions for human review. These systems integrate with core banking platforms, payment processors, and general ledger systems to create seamless data flows.

Benefits of automation include:

- Reduced manual effort and associated labor costs

- Faster close cycles enabling more timely financial reporting

- Enhanced accuracy through elimination of manual data entry errors

- Improved audit trails and compliance documentation

- Real-time visibility into reconciliation status

Data Extraction and Transformation

Accounting teams frequently need to extract data from PDF bank statements and other documents that exist in non-structured formats. Modern solutions use artificial intelligence to recognize transaction patterns and convert these documents into spreadsheet formats that integrate with accounting systems.

This capability proves especially valuable when dealing with correspondent bank statements, investment account reports, or legacy systems that don't provide direct data feeds.

Internal Controls and Audit Considerations

Robust internal controls represent a cornerstone of effective accounting in bank operations, protecting against errors, fraud, and regulatory violations.

Segregation of Duties

Banking institutions implement strict segregation between transaction initiation, approval, recording, and reconciliation functions. This fundamental control prevents any single individual from having end-to-end control over financial processes.

Typical segregation includes:

- Loan origination staff cannot approve loans

- Cash handling employees cannot perform vault reconciliations

- Wire transfer initiators require separate authorization

- Journal entry preparers need supervisory approval

- Reconciliation performers work independently from transaction processors

External Audit Requirements

Banks face rigorous external audit requirements beyond typical commercial entities. Auditors examine not only financial statement accuracy but also the effectiveness of internal controls over financial reporting.

The audit process for bank accounting practices typically encompasses:

- Risk assessment and audit planning

- Internal control evaluation and testing

- Substantive testing of account balances

- Loan portfolio review and loss allowance validation

- Securities valuation and classification verification

- Regulatory capital calculation review

- Compliance testing for applicable regulations

Advanced Accounting Topics for Complex Instruments

Larger banking institutions deal with sophisticated financial instruments requiring specialized accounting knowledge and systems.

Derivative Instruments and Hedging

Banks use derivatives to manage interest rate risk, foreign exchange exposure, and other market risks. Hedge accounting allows entities to match the timing of gains and losses on derivatives with the risks being hedged.

The three types of hedges each have distinct accounting treatments:

Fair value hedges: Protect against changes in the fair value of assets, liabilities, or firm commitments. Both the derivative and hedged item are marked to market through earnings.

Cash flow hedges: Guard against variability in future cash flows. The effective portion of derivative gains and losses is recorded in other comprehensive income until the hedged transaction affects earnings.

Net investment hedges: Hedge foreign currency exposure in foreign operations, with treatment similar to cash flow hedges.

Mergers and Acquisitions Accounting

Bank consolidation remains common, requiring proper application of business combination accounting under GAAP. The acquisition method involves:

- Identifying the acquirer and acquisition date

- Measuring total consideration transferred

- Recognizing and measuring identifiable assets acquired and liabilities assumed at fair value

- Recognizing goodwill or bargain purchase gain

Intangible assets like core deposit relationships, customer relationships, and favorable lease agreements require separate identification and valuation, adding complexity to the purchase price allocation.

Regulatory Capital Accounting

Beyond traditional financial accounting, banks must calculate regulatory capital ratios that determine their ability to operate, grow, and pay dividends.

Capital Components and Risk Weighting

Regulatory capital consists of Common Equity Tier 1 (CET1), Additional Tier 1, and Tier 2 capital. Each category has specific inclusion criteria and limitations.

Risk-weighted assets apply different risk percentages to various asset classes:

| Asset Category | Risk Weight | Reasoning |

|---|---|---|

| Cash and Treasury securities | 0% | No credit risk |

| Residential mortgages | 50% | Moderate risk with collateral |

| Commercial loans | 100% | Standard credit risk |

| Past due loans | 150% | Elevated default risk |

| Equity investments | 300%+ | High volatility and risk |

Understanding these calculations helps accounting professionals see how balance sheet composition affects regulatory capital adequacy and strategic options.

Professional Development and Education

Given the specialized nature of accounting in bank environments, continuous education remains essential for accounting professionals in the industry. Organizations like the Wisconsin Bankers Association offer comprehensive training that goes beyond basic GAAP to address banking-specific accounting challenges.

Topics that deserve focused study include:

- Credit risk modeling and CECL implementation

- Complex financial instrument accounting

- Regulatory reporting requirements and deadlines

- Technology tools for automation and efficiency

- Emerging accounting standards and their banking implications

Staying current with common questions about banking operations and accounting treatment ensures professionals can adapt to industry changes and maintain compliance.

Risk Assessment Through Accounting Metrics

Financial accounting data provides critical inputs for risk management and early warning systems. Research on bank failures demonstrates that deteriorating accounting metrics often precede banking crises, making proper interpretation of financial data essential for stability.

Key Performance and Risk Indicators

Bank management and regulators monitor numerous ratios derived from accounting data:

Profitability metrics:

- Return on assets (ROA)

- Return on equity (ROE)

- Net interest margin

- Efficiency ratio

Asset quality measures:

- Non-performing loans ratio

- Net charge-off rate

- Loan loss reserve coverage

- Criticized and classified loans ratio

Capital adequacy:

- Tier 1 leverage ratio

- Common Equity Tier 1 ratio

- Total risk-based capital ratio

Liquidity indicators:

- Liquidity coverage ratio

- Net stable funding ratio

- Loan-to-deposit ratio

These metrics transform raw accounting data into actionable insights about institutional health and risk exposure.

Understanding accounting in bank operations requires mastery of specialized standards, regulatory frameworks, and complex financial instruments that distinguish banking from other industries. From loan loss provisioning under CECL to derivative hedge accounting, banking professionals navigate unique challenges that demand continuous learning and adaptation. Bank Statement Boss streamlines the data preparation process by converting PDF statements into structured spreadsheet formats with 99% accuracy, integrating seamlessly with major accounting platforms while maintaining bank-level security. This automation allows accounting teams to focus on analysis and strategic decision-making rather than manual data entry, improving efficiency across the financial reporting cycle.